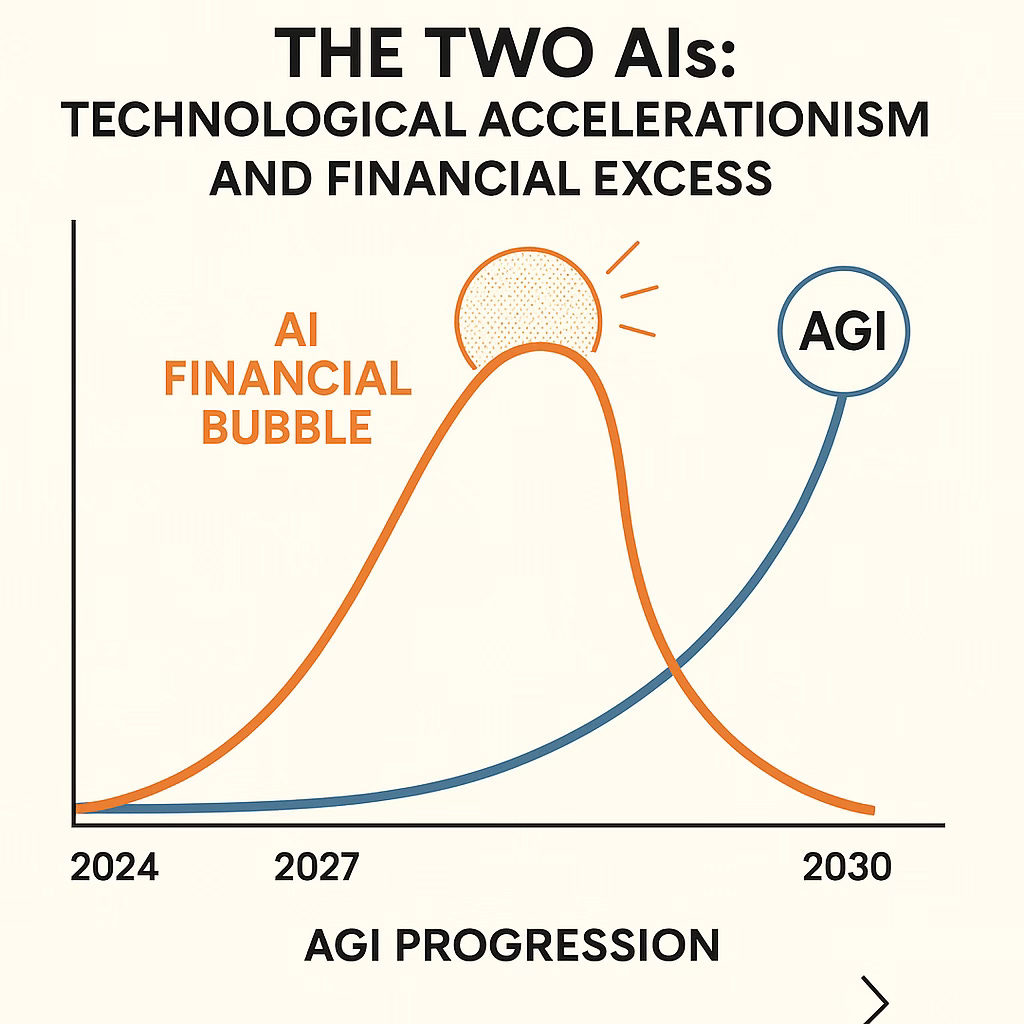

The Two AIs: Technological Accelerationism and Financial Excess

A future in which the AI bubble bursts in 2027 but AGI emerges by 2030 is logically consistent.

Public debate around artificial intelligence has become trapped in a false binary that conflates two distinct but interdependent phenomena: AI as a technological revolution and AI as a financial bubble. These forces are deeply intertwined; speculative enthusiasm channels capital into genuine innovation, while technological progress amplifies market exuberance. Yet they remain fundamentally different. Their interaction defines the present moment, but public discourse persistently merges them into a single story, obscuring both the substance of the technology and the logic of the bubble.

Even if the world were to reach something approximating artificial general intelligence by around 2030, a timeline that remains speculative and depends on how one defines the term, that breakthrough would not necessarily vindicate today’s market exuberance. ‘AGI’ is less a scientific milestone than a cultural shorthand for a far more capable and autonomous form of AI, and its meaning continues to evolve with the technology. What is certain is that financial belief moves faster than physics or computation. Capital can multiply overnight through speculation, while the material foundations of progress—data, hardware, energy, and research—advance at a slower, physical pace. What we are witnessing, therefore, is not only a genuine acceleration in technological capability but also a cycle of speculative excess that, paradoxically, is financing the infrastructure likely to enable AI’s more profound and more enduring transformation.

The evidence for AI’s genuine, measurable progress is mounting across markets, firms, and individuals. Global spending on artificial intelligence, including software platforms, hardware such as AI chips and servers, and related services like cloud deployment and consulting, totaled roughly $244 billion in 2025 and is projected to grow to around $827 billion by 2030.

Behind this trend is a dramatic expansion in computational scale, driven by the Scaling Law for AI. This law shows a clear, predictable link between resource investment and model capability: training compute for frontier models has doubled every six months since 2018, an order of magnitude faster than Moore’s Law. This rapid escalation in compute has been justified by equally consistent gains in intelligence, versatility, and accuracy.

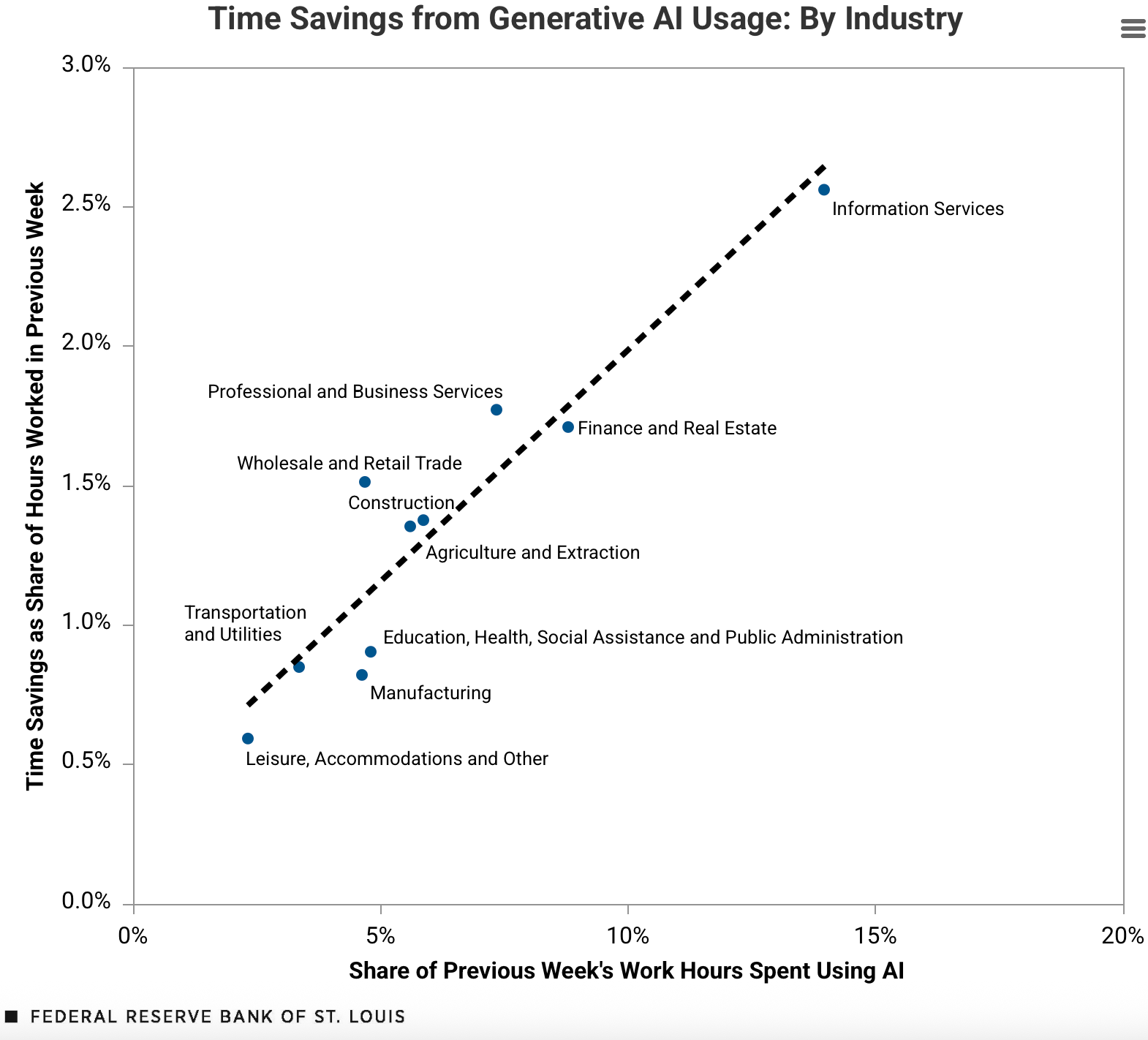

Forecasts from major institutions vary in magnitude but not in direction: all anticipate a substantial uplift in productivity and output. Goldman Sachs projects that generative AI could raise global GDP by 6-7 percent over the next decade, while PwC estimates a broader boost of around 10–14 percent by 2030. McKinsey offers an even higher range, forecasting that AI could expand global output by roughly 13–20 percent by the end of the decade, driven by automation, accelerated innovation, and the spread of efficiency gains across industries. The mechanisms behind these projections are already visible. A 2025 Federal Reserve study found that workers using generative-AI tools saved 5.4 percent of their work hours, translating into a 1.1 percent rise in aggregate productivity. At the firm level, analyses show total-factor-productivity gains of 2–3 percent, indicating that AI is enabling organizations to generate more value from the same mix of labour and capital, the essence of sustainable growth. The IMF reports task-level efficiency improvements ranging from about 14 percent for lower-skilled roles to over 50 percent for software engineers, illustrating how AI scales across the skill spectrum. As firms reinvest these time and cost savings into new activity, efficiency compounds throughout the economy, raising not only output but also the underlying capacity for long-run prosperity.

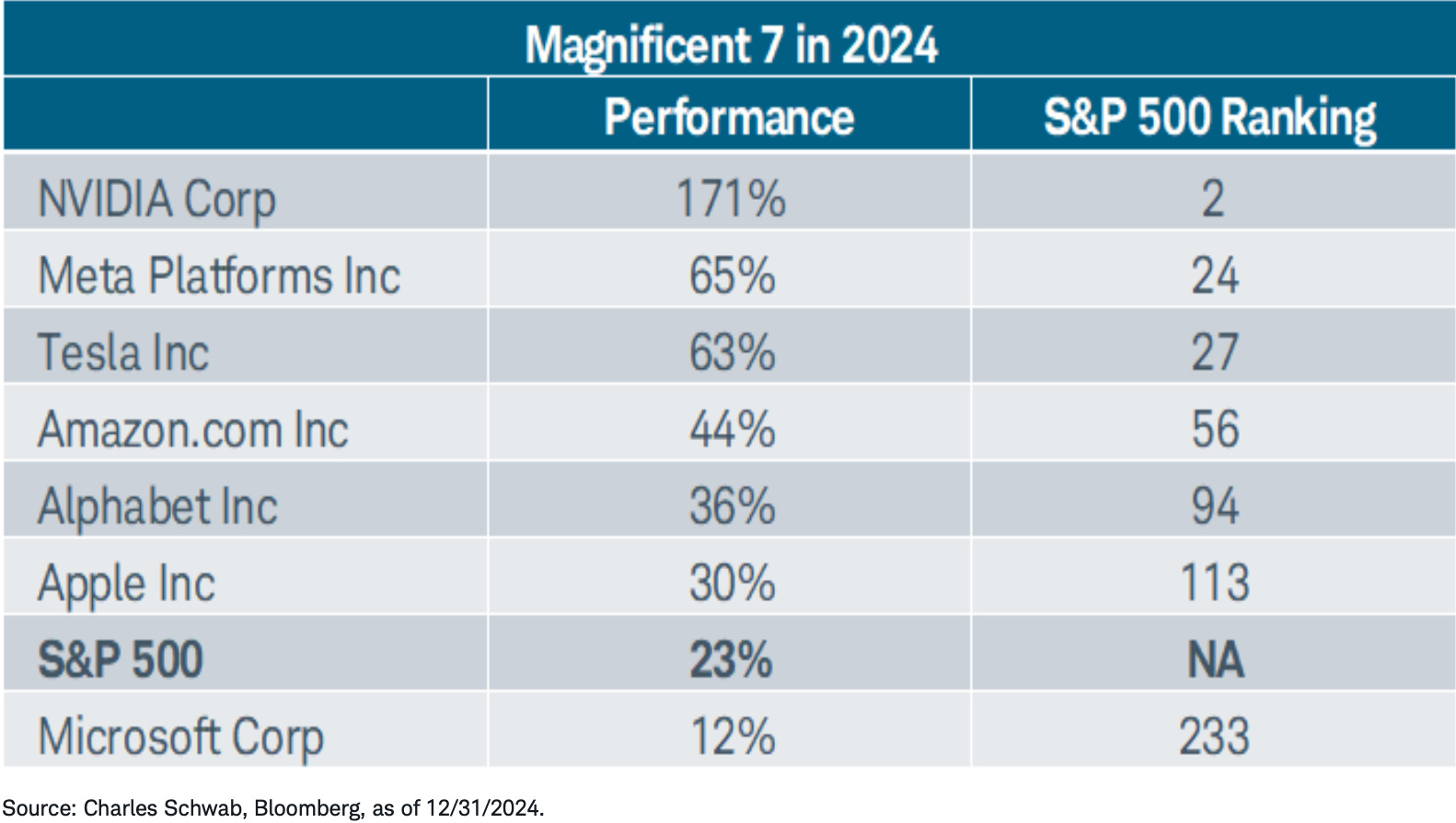

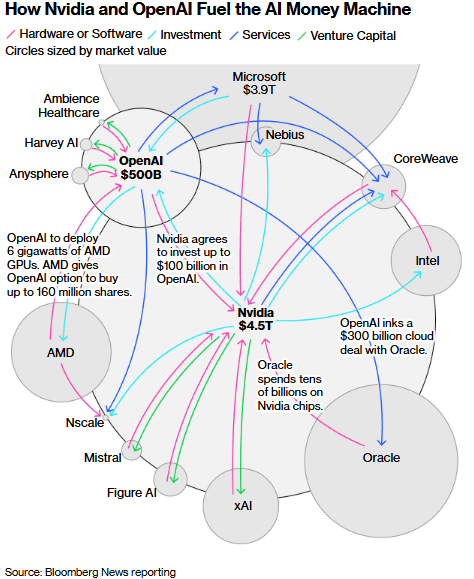

If AI’s technological progress has been rapid, its financial ascent has been extraordinary. By late 2025, artificial intelligence had become the gravitational centre of global capital markets, driving valuations to levels unseen since the dot-com era. Roughly 30 AI-linked companies now account for about 44% of the S&P 500’s total market value, a degree of concentration unprecedented in modern markets. Within that group, the most prominent firms, Nvidia, Microsoft, Alphabet, Amazon, and Meta, alone represent close to a third of the index’s weight. Nvidia, valued at around $4.4 trillion, stands as the world’s most valuable or second-most-valuable company, larger than the entire German equity market and emblematic of investors’ belief in AI’s long-term profitability. Analysts estimate that most of the S&P 500’s cumulative gains since 2023 have been powered by these same giants, while the average stock has lagged sharply behind: the equal-weight S&P rose only 10% in 2024 versus 25% for the cap-weighted benchmark. The surge has radiated outward to other chip and cloud suppliers, TSMC, Broadcom, AMD, Oracle, and Palantir, whose combined market capitalisations add several trillion dollars more. The result is a market increasingly dominated by a narrow cluster of firms whose valuations and fortunes hinge on the same AI narrative.

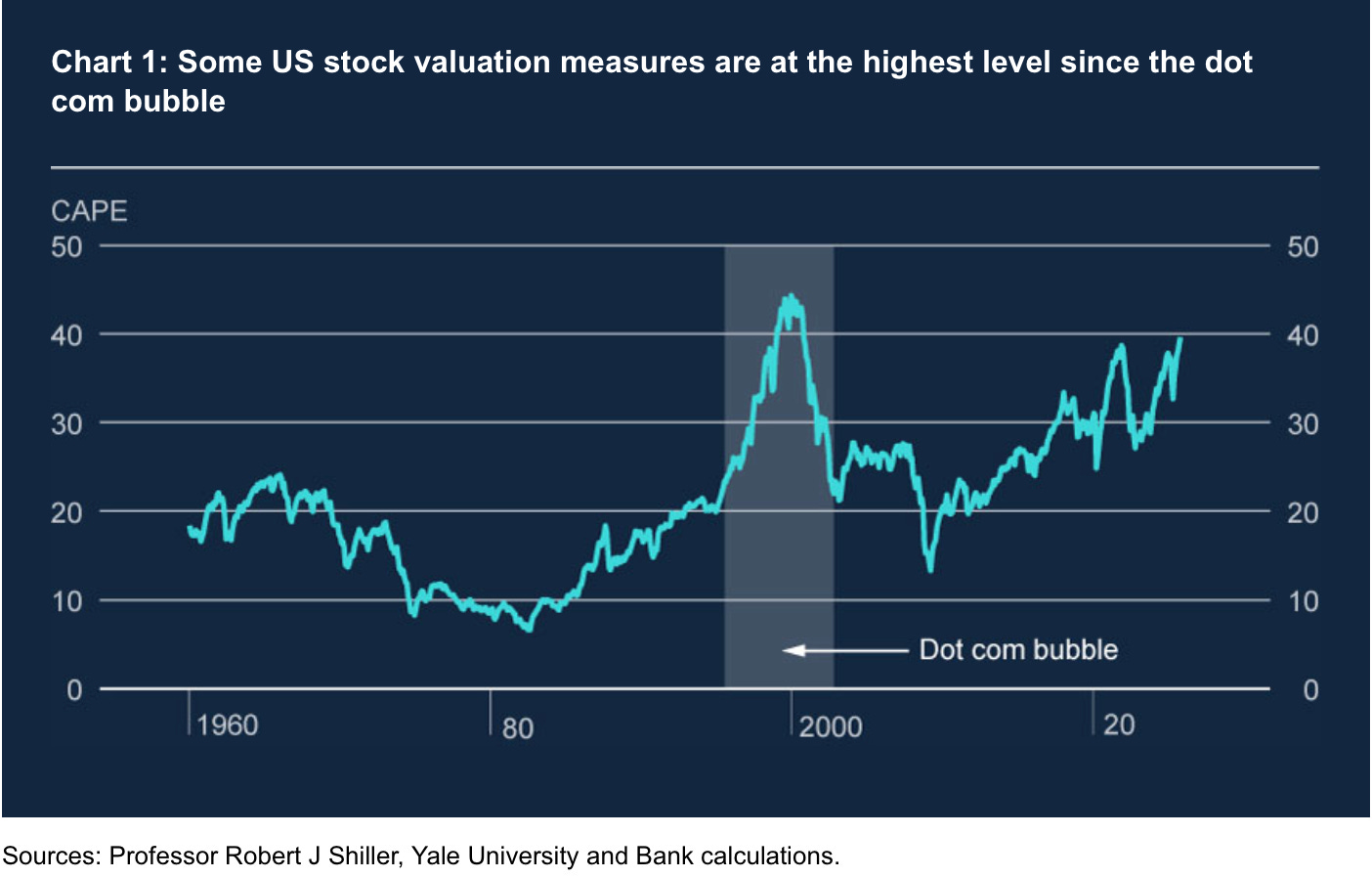

The comparison with the late-1990s internet boom is unavoidable: markets are once again pricing in a technological transformation long before its profits have fully materialised. During the peak of the dot-com era, the NASDAQ Composite surged roughly 400–500% before collapsing 77% by 2002, as valuations built on future promise proved unsustainable. Then, as now, speculative capital chased a general-purpose technology, first the internet, now artificial intelligence, believed to reshape production and work. Yet the parallels are not perfect. Unlike the loss-making start-ups of 2000, today’s AI-linked giants are generating immense cash flow from cloud computing, advertising, and semiconductor sales. One recent analysis found that among S&P 500 firms with measurable AI exposure, six of nine already derive most of their revenue from AI-related product lines. The physical infrastructure underpinning this boom, data centres, advanced chips, and high-performance computing networks, is visibly expanding, drawing real-economy investment on a scale unseen in the earlier era.

Even so, the dynamics of speculative excess are unmistakable. Valuations have outpaced even the most bullish earnings-growth projections, and markets increasingly treat any mention of AI as a reason to reprice higher, regardless of substance. The feedback loop between rising valuations and investor conviction has tightened into a reflexive cycle: higher prices reinforce belief in AI’s inevitability, attracting more capital and pushing valuations higher still. This concentration creates the illusion of broad prosperity while revealing how dependent the U.S. economy has become on a single growth engine. Corporate profits, household portfolios, and tax revenues have all been buoyed by AI-driven equity appreciation, cushioning the drag from higher interest rates and weaker demand elsewhere. Strip away these firms, and the S&P 500’s performance over the past two years would look far more ordinary. AI’s financial shadow now stretches across the entire economy, its promise sustaining valuations, and those valuations in turn financing the infrastructure and research needed to make that promise real.

Whether this constitutes a ‘bubble’ depends on one’s definition. In the classical sense, a speculative rise untethered from fundamental value, parts of the AI trade exhibit all the hallmarks: extreme market-cap concentration, stretched valuations, and narrow breadth. Yet unlike the dot-com era, the foundations are not wholly imaginary. As previously referenced, AI is already boosting productivity, reducing costs, and generating measurable returns. What seems inflated, then, is not AI’s eventual impact but the speed and scale that markets have priced in

The financing structure of the AI boom has evolved with extraordinary speed, heightening both its durability and its potential volatility. What began as an equity-led rally in a few dominant tech firms has become a dense lattice of cross-financing among chipmakers, hyperscalers, venture funds, and AI start-ups, where capital circulates in a self-reinforcing loop. Nvidia’s surging profits finance new capacity and ecosystem R&D, while its customers—Microsoft, Amazon, Google, Meta, and a swelling constellation of model builders—commit ever-larger sums to GPUs, data centres, and AI infrastructure, effectively recycling one another’s revenues. This has raised valuations across the sector and embedded AI spending into corporate capex, sovereign portfolios, and government budgets, meaning any valuation shock would now echo far beyond markets.

A meaningful correction could emerge in mid-to-late 2026, when capacity expansion, cost saturation, and investor fatigue may collide: GPU supply is projected to overtake near-term demand, margins could flatten as competition intensifies, and earnings growth may begin to lag the capital already deployed. In that scenario, valuations might retrace 20–40% as the market digests its own exuberance. Yet several alternate paths remain plausible. A rolling correction, in which capital rotates from semiconductors to software to application-layer firms, could diffuse systemic impact while preserving overall market enthusiasm. Conversely, if AI capability breakthroughs (e.g., autonomous agents, on-device inference, or advanced reasoning models) accelerate commercial adoption faster than expected, the current boom could extend well into 2027, supported by rising profits and infrastructure monetisation. The likely outcome is neither a decade-long collapse nor endless ascent, but oscillation, a series of sharp months-long repricing periods within an enduring long-term bull cycle.

Whether or not a correction comes soon, the broader lesson is clear: the world’s confusion between AI as a technological revolution and AI as a financial bubble distorts our view of both. These are intertwined yet distinct forces, moving on different clocks but feeding the same story. The technological side is slow, cumulative, and grounded in measurable gains in productivity and infrastructure; the financial side is fast, reflexive, and driven by narrative and capital flows. Both can be true at once: speculation accelerates innovation even as it exaggerates it, while innovation sustains speculation by giving it substance. But failing to distinguish between the two carries real costs. It blinds individuals, firms, and nations to the true pace of technological progress, leaving them unprepared for how quickly AI will reshape competition, productivity, and power. At the same time, it lulls investors into mistaking financial euphoria for stability, ignoring that every acceleration cycle breeds its own volatility. When valuations inevitably correct, many will misread a temporary financial downturn as a technological failure, pulling back just as the next wave of breakthroughs begins to crest. The result is a self-inflicted setback: capital fleeing too early, policy turning cautious, and public sentiment souring on a revolution still compounding beneath the surface. The danger lies at both extremes: to underestimate AI’s trajectory is to fall behind, but to overestimate its immunity to financial gravity is to court ruin. Clarity means guarding against both, recognizing that the bubble and the breakthrough are not opposites but partners in motion.

Fitting that you posted this October 29th. Tuesday, Oct 29th 1929 was of course Black Tuesday.

The PE ratios had gotten to 66:1. Mass speculation, with government and wall street cheering it on.

Eventually, gravity takes hold.

When new industries emerge — automobiles, planes, internet companies, AI companies — a lot of investment comes pouring in. A hundred new companies are formed, all vying for that future market. 100 car companies became 3. That’s a mature market. Fortunes are lost as well as made along the way.

You are right to note that in AI’s case at least, the speculative bubble will leave a platform for AI’s continuing evolution once the dust settles.